Better, faster, cheaper: Multibank tokenization networks could transform cross-border payments

Transaction costs and delays in processing payments often strain banking relationships with business customers. Here are steps banks can take to help ease the pain.

Roy Ben Hur

CJ Burke

Zachary Aron

Jill Gregorie

Shivalik Srivastav

Businesses are calling on banks to offer faster and more efficient cross-border payment capabilities. These organizations may encounter high transaction costs, slow payment speeds, and unclear settlement times when moving money internationally, which can hamper their relationship with banking partners.1 At the same time, fintechs appear poised to continue capturing a larger share of the cross-border payment market by offering user-friendly services and lower fees.2

Many government and market initiatives are underway to assess how digital forms of money can be more quickly and securely transferred across borders. By tokenizing regulated assets such as commercial bank deposits and central bank deposits, payment processors could make round-the-clock transactions that settle instantly on a unified ledger. The 24/7 movement of tokenized currencies will likely require fewer handoffs between intermediaries, generating significant reductions in transaction costs.3

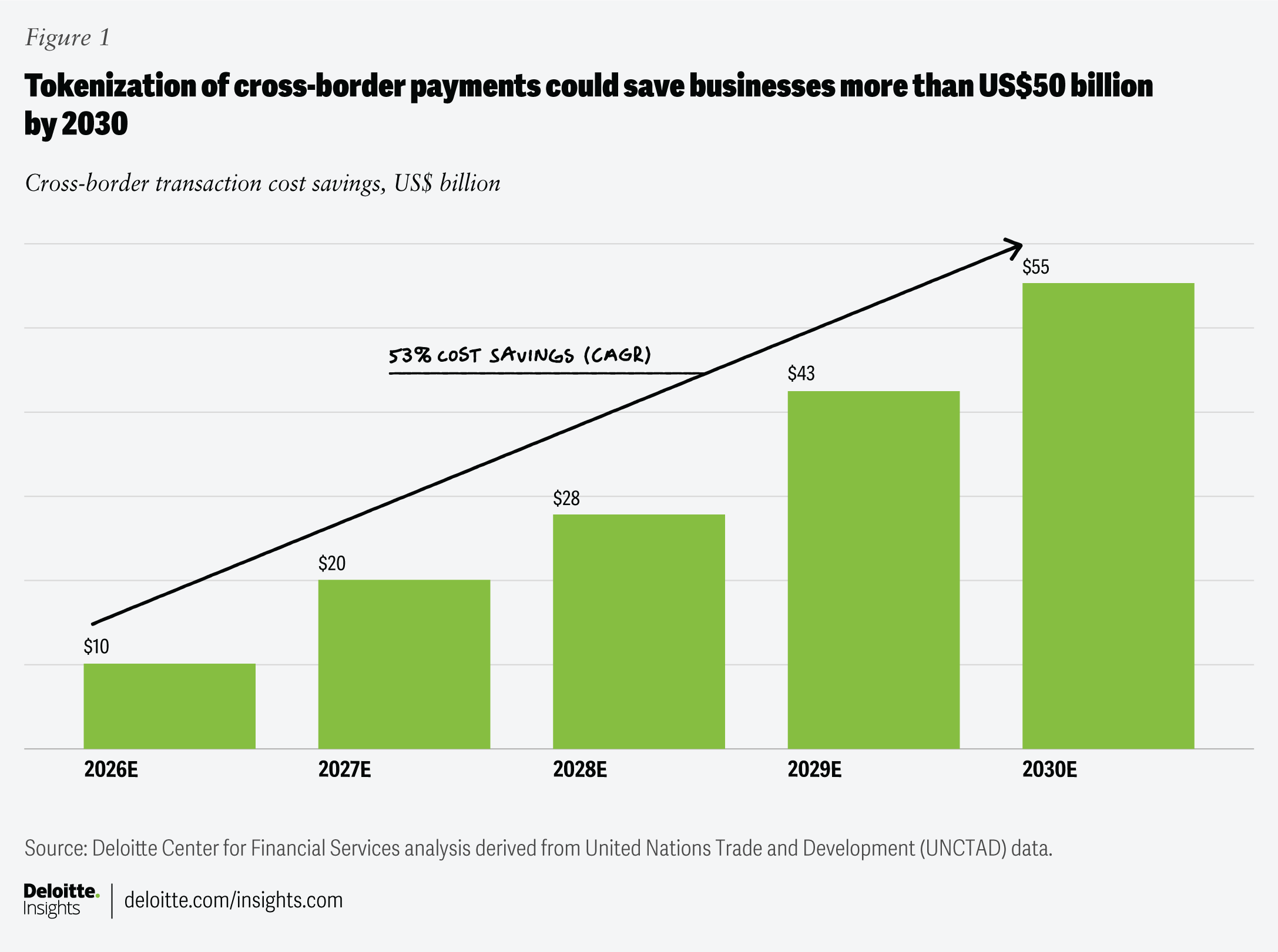

Major banks are banding together to strengthen tokenized currency networks to process global real-time payments. The Deloitte Center for Financial Services predicts that 1 in 4 large-value international money transfers will settle on these platforms by 2030.4 The efficiencies gained by advancements in tokenized payment infrastructure should lower the cost of corporate cross-border transactions by 12.5%, which would save business customers over US$50 billion by 2030 (figure 1).5 (See “About this prediction.”)

{kind=link}

Why cross-border payments could remain a cross-border headache

Wholesale payments—large-value transactions exceeding US$100,000—comprise the bulk of cross-border transaction volumes.6 Most wholesale payments flow through a network of correspondent banks that connect financial institutions to foreign markets where they lack a local presence. While transactions between major markets typically use one correspondent bank to process payments, some may require multiple intermediaries to manage more exotic currency conversions. Each correspondent bank is responsible for updating balances in the accounts of banks that precede and follow it. Since this typically occurs during the normal business hours of each bank’s respective domestic payment system, settlement delays may be particularly lengthy between countries with large time-zone differences.7

Recent industry initiatives, including Swift’s enhancements to payment tracking and The Clearing House’s pilot program for instant payments between the United States and Europe, are advancing payment modernization.8 But cross-border payments that require multiple correspondent relationships can still be cumbersome. Their transaction costs also tend to be higher since each intermediary may impose fees for processing, settlement, and foreign exchange.9 As a result, originating banks may need to commit additional funding to cover unexpected expenses or high foreign exchange spreads.10 In addition, multiple compliance and validation checks can lead to settlement delays that immobilize bank funds or tie up corporate customers’ working capital.11

Banks can band together to help alleviate pain points

Tokenization of cross-border payments could help reduce compliance costs since security checks can be built directly into transaction flows by prevalidating originator and recipient details. Unlike conventional transactions that send payment instructions separately from funds, blockchain-based transfers of tokenized currencies may reduce information gaps by integrating messaging with money movement. For instance, banks can program smart contracts to automatically execute payments when live data confirms certain conditions are met.

One source of competitive differentiation could stem from the tokenized currencies each platform supports. These digital cash instruments may include stablecoins, which are issued by a bank or private entity and pegged to a single asset, such as the US dollar; tokenized commercial bank deposits, which represent traditional bank deposits; and tokenized central bank deposits, which are regulated by jurisdictions and backed by central bank reserves.

Multibank networks being put forth by the private sector could become the predominant venue for cross-border payments using tokenized currencies by 2030. Bank consortiums are already piloting new settlement systems and refining methods for exchanging tokenized currencies on a common ledger.12 These banks are likely to converge on shared networks when global regulators establish clear frameworks for the use of digital assets.

Stablecoins emerge as a near-term frontrunner

Stablecoins may offer a clear path forward for wholesale cross-border payments in the near term. The United States is expected to follow other jurisdictions in advancing legislation on stablecoins; recent draft bills in Congress have received bipartisan support.13 President Trump has also called on federal agencies to spur the growth of “lawful and legitimate dollar-backed stablecoins” in a January executive order.14 These measures could foster widespread acceptance of stablecoins and accelerate banks’ adoption of stablecoin-based payment solutions.15

Consequently, networks that enable the transfer of highly trusted stablecoins are likely to achieve significant market penetration over the next five years. Banks may coalesce around emerging blockchain platforms or rely on existing networks, such as The Clearing House and Swift, to exchange their proprietary coins with other institutions. These arrangements will likely follow an approach known as a “stablecoin sandwich,” where a bank converts the local currency to a stablecoin and instantly transfers it to another bank on a blockchain network, and the recipient bank credits the beneficiary account in its domestic currency.16

Some banks and fintechs are also collaborating with regulators to research technical specifications, governance standards, and controls that can safeguard participants on public, permissionless blockchain networks.17 These open networks could get a boost from President Trump’s endorsement of public ledgers for stablecoins and other tokenized assets.18 In addition, emerging payment networks may invest in application programming interfaces, portals, and gateways that can make it easier to onboard banks and settlement agents, which could expand the number of countries and currencies supported by real-time payment capabilities.

Several global banks have started trialing cross-border payments on shared ledgers using tokenized versions of traditional currencies. In late 2023, transactions went live on Fnality, a UK-based payment system that links domestic payment and settlement systems with a blockchain platform that exchanges bank-agnostic tokens, called utility settlement coins, which represent digital cash.19 These coins have attributes of tokenized central bank deposits because banks can only access them by funding an associated central bank account.20

Some governments are also working with banks to develop a single settlement system for traditional and tokenized currencies. For example, the Institute of International Finance gathered seven central banks and 41 financial institutions to cooperate on Project Agorá, a public-private partnership led by the Bank for International Settlements.21 The collaboration expects to deliver a working prototype for multicurrency transfers on a unified ledger.22 The project plans to complete technical research by the end of 2025.23

Regulatory and tech challenges could impede progress

Legal and technical challenges could slow the pace of development and adoption of industrywide solutions. Regulatory frameworks for tokenized assets and blockchain-based transactions are still emerging. These include blockchain interoperability standards, permissible forms of digital money, and requirements for ledger participation.24

Another challenge could stem from synchronizing digital ledgers with legacy domestic settlement networks. A large share of settlement systems still run on decades-old technology that was built when paper processes first migrated to electronic platforms.25 These legacy systems may have functional limitations that constrain data- and asset-sharing.

The race to real-time payments accelerates

The following are steps banks could consider to help operationalize tokenized networks.

1) Assess the operational impacts of moving transaction flows to the blockchain, identifying where financial and technical risks may warrant improved process controls.

2) Bolster security protocols to safeguard corporate customers that want to be early movers in stablecoin-based transactions.

3) Identify target cross-border payment channels and segments for initial transactions, prioritizing those with the highest degree of adaptability, the fewest number of intermediaries, and an extensive history of cooperation.

4) Strengthen internal capabilities for new offerings with tokenized payments and develop value-added services, such as programmable payments and real-time liquidity services.

5) Continue to experiment and collaborate with industry groups to reduce inefficiencies in the underlying ledger technology. Banks can also partner on research and technologies for digital identity management and work with regulatory agencies to establish shared standards for data privacy and security.

The race to real-time payment capabilities is accelerating. Banks that wait on the sidelines may find themselves at a competitive disadvantage to others that get there first. To help maintain strong relationships with corporate customers, banks should continue to push forward with innovative payment solutions, strategic partnerships, and value-added services for cross-border transactions.

About this prediction

Our prediction for cross-border payments is based on data and input for transaction volumes and fees from Deloitte specialists in payments, tokenized assets, and ledger-based financial infrastructure. We forecast the market size for corporate wholesale cross-border payments in North America, Europe, and Asia through 2030. We applied the expected level of cost savings to the share of corporate cross-border payments that should be made with tokenized assets by 2030. While these trade-related and investment-related transactions comprise a large share of wholesale cross-border payment flows, banks could also realize savings when conducting cross-border activities, such as foreign exchange. Assumptions made in the forecast are informed by our understanding of industry pilots and institutional readiness for token-based payment systems.

This article contains general information and predictions only and Deloitte is not, by means of this article, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This article is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor.

Deloitte shall not be responsible for any loss sustained by any person who relies on this article.